A New Type of Audit?

By Jacek Mazur

„Kontrola Państwowa” No 6/2020

Supreme Audit Institutions (SAIs) strive to address important and topical concerns which attract media coverage and are of interest to the Parliament and citizens. Since 2013, the National Audit Office of the United Kingdom (NAO) has been carrying out ‘Investigations’. These are not investigations as defined in criminal law but rapid and responsive ‘engagements’ with data gathered and presented quickly. The topics of such investigations are specific, so that they can be developed fast (usually within three-four months) and described briefly (reports should not exceed 5,000 words). Investigations usually address issues that give rise to social concerns that things might not work properly, so their main addressees are not state bodies, but citizens, too. Unlike in financial and performance audit, investigations are facts only (without evaluations or recommendations), however they are written in a way that allows the readers to draw their own conclusions. In this article, the author discusses changes impacting on the NAO and its work supporting the House of Commons, and presents the concept and practice behind these. The role of such investigations is viewed in the context of other NAO activities, the topics covered and procedures adopted.

National Audit Office of the United Kingdom

System Evolution

The contemporary British public audit system was established some 150 years ago: in 1866 ministries were obliged to prepare annual accounts to benchmark expenditure against the resources they were granted, and to submit their accounts to the Public Accounts Committee (PAC - a select committee of the House of Commons). The position of Comptroller and Auditor General (hereinafter referred to as the C&AG) was also established to combine authorisation of the issue of money to departments (the comptroller function) and the examination of accounts (the auditor function).

Generally, rules have remained the same to this day: Parliament adopts the budget, the ministries act, spend money, and present accounts; the C&AG conduct audits, the Public Accounts Committee draws on the C&AG’s work to hold government officials to account for the economy, efficiency and effectiveness of public spending. After each evidence session, the PAC publishes a report setting out its findings and recommendations[1]. However, changes have also been introduced. The Act of 1866 required the C&AG and his / her staff to examine every transaction, which - due to expanding governmental activities (especially after the First World War) - became less and less feasible. As a result, the first systemic change was introduced: the Act of 1921 allowed for verification of selected transactions only, and permitted to use the ministries’ own control mechanisms. The other important change was introduced after the Second World War, when - apart from certification audits - the administration’s activities started to be audited with regard to economy, efficiency and effectiveness (performance audit, which in the United Kingdom is referred to as value for money audit) - initially without a statutory mandate, on the basis of a widened interpretation of the certification audit. It was only after the introduction of the Act of 1983[2] when the C&AG was granted a clear legal basis to conduct value for money audits.

New Structure of the Audit Body

The British national audit system as at the end of the 20th century has been described in several earlier publications[3]. With the Act of 2011[4] came reform: a new approach to the governance and management of the National Audit Office and extended impact of the House of Commons.

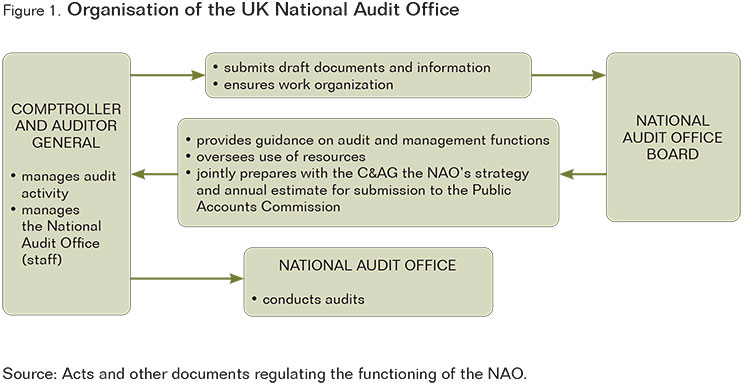

Since 2012, a one-person body with reporting staff has been replaced by two interrelated bodies: the Comptroller and Auditor General (supported by the National Audit Office) and the NAO Board (see Figure 1).

Figure description

Figure 1. Organisation of the UK National Audit Office

COMPTROLLER AND AUDITOR GENERAL

- manages audit activity

- manages the National Audit Office(staff)

COMPTROLLER AND AUDITOR GENERAL to NATIONAL AUDIT OFFICE BOARD

- submits draft documents and information

- ensures work organization

NATIONAL AUDIT OFFICE BOARD to COMPTROLLER AND AUDITOR GENERAL

- provides guidance on audit and management functions

- oversees use of resources

- jointly prepares with the C&AG the NAO’s strategy and annual estimate for submission to the Public Accounts Commission

NATIONAL AUDIT OFFICE

- conducts audits

Source: Acts and other documents regulating the functioning of the NAO.

The Comptroller and Auditor General manages the audit activity: the C&AG is charged with examining the accounts and activities of the administration and other entities that use public funds, as well as submitting the results thereof to the Public Accounts Committee. The position of the C&AG remains strong: it is appointed by The Queen upon an address to the House of Commons by the Prime Minister, who can only act with the consent of the Chair of the Public Accounts Committee - usually a member of the opposition party (such an arrangement has been in operation since the 19th century and has been designed to obtain the consent of the two main parties). However, a term of office of ten years has been introduced and it cannot be extended; previously the term was unlimited. The C&AG can be dismissed by a joint motion of the two Houses of the Parliament, although this has never happened and an unlikely eventuality. The Act of 2011 confirms the principle of the C&AG as ”an officer of the House of Commons”; this being a titular concept to underline his / her independence, since officers of the House of Commons are not answerable to the government. It is also a title which stresses the service role of the C&AG which he / she performs for the House of Commons (conducting audits on its behalf), and confers the right of unlimited access to the House. The C&AG decides on audit topics, procedure and methodology, having regard to any recommendations made by the Public Accounts Committee. The C&AG has the right to independently decide on value for money examinations: the number of audits and their topics, the manner for their conducting, the contents of reports and whether and in what way they are submitted to the House of Commons. The Act does not set out the audit procedure or methodology (it only regulates the right to access documents); in financial auditing the generally binding accounting standards are applied, while in value for money audits - the NAO’s own principles, which are compliant with the international guidance on public audit.

The NAO Board[5] supports the Comptroller and Auditor General by advising and monitoring him / her, as it judges appropriate, in the exercise of the C&AG’s functions: the Board must, in such manner as it considers appropriate, monitor the carrying out of the C&AG’s functions and may provide advice (the Comptroller and Auditor General must have regard to any advice given). The NAO Board also oversees the management of the NAO’s resources and monitors the achievement of performance objectives; it co-authors the annual activity report and draft NAO’s strategies and budgets, it co-decides on the Code of Practice in relation to the relationship between the C&AG and the Board, and it can authorise the C&AG to conduct activities other than those set forth in legislation - for example, discretionary services relating to international cooperation[6]. The NAO Board is composed of five non-executive members (one of them is Chair), and four executive members: the C&AG and three NAO staff members. The Chair of the NAO Board is appointed under the same procedure as the C&AG (i.e. by The Queen upon an address by the Prime Minister, agreed on with the Chair of the Public Accounts Committee); this helps to ensure high authority and independence. The other non-executive members are appointed by the Public Accounts Commission of the House of Commons following a recommendation by the Chair of the NAO Board, while NAO staff members are appointed by the NAO Board - upon a recommendation by the C&AG. The NAO Board gathers at plenary meetings (usually seven meetings a year). In addition, the NAO Board has two committees composed of non-executive members: the Audit and Risk Committee (systems of internal control, risk management and corporate governance) and the Remuneration and Nominations Committee (framework for the remuneration of the three executive members, overseeing major changes in NAO’s employee benefits).

The NAO governance model is based on established private sector good practice. As the NAO’s website reads: ”The NAO’s governance arrangements reflect our statutory position, balancing the need for appropriate controls and oversight against the preservation of the Comptroller & Auditor General’s independence”[7].

Relationship with Parliament

The National Audit Office supports the House of Commons in holding government to account in spending public money. The House of Commons is involved in the appointment and dismissal of the separate posts of Comptroller and Auditor General and the Chair of the NAO Board (both posts are Crown appointments), and other non-executive Board members, as well as - through the Public Accounts Commission[8] - overseeing the NAO’s work, scrutinising its performance and approving the NAO’s strategy and annual estimate.

Over the last years, relations between the National Audit Office and the House of Commons have developed further, both with regard to the practice evolution, and legal changes. The Act of 2011 expanded parliament’s supervision mandate: nowadays the Public Accounts Commission approves the documents that regulate the NAO operations: inter alia, the Code of Practice in relation to the relationship between the C&AG and the Board, the rules for delegating the C&AG’s responsibilities to NAO staff members, and potential audits fees. Furthermore, the C&AG is obliged to have regard to value for money topics suggested by the Public Accounts Committee.

Figure description

Figure 2. Relations between the National Audit Office and Committees of the House of Commons

PUBLIC ACCOUNTS COMMISSION

- oversees the work of the NAO and scrutinises its performance

- approves the NAO’s budget and strategy

- approves the documents that regulate NAO operations

- appoints non-executive members of the NAO Board

- approves an auditor for NAO for each financial year

PUBLIC ACCOUNTS COMMITTEE

- has the right to examine the NAO’s audit reports

- drawing on the NAO work, holds government officials to account for the economy, efficiency and effectiveness of public spending

- looks at how public money has been spent and does not examine the merits of government policy

- is entitled to propose value for money audit topics that the NAO must have regard to into account

- can submit comments on the NAO’s draft budget

- the NAO submits to the Committee audit reports and participates in their examination

DEPARTMENTAL SELECT COMMITTEES

- a Commons Select Committee exists for each government department, examining spending, policies and administration

- they may call in officials and experts for questioning, and can demand information from the government

- the NAO has discretion to provide formal and informal advice, as well as documents in response to committees’ questions

- the NAO produces overviews of departments, summarising their responsibilities, how they spends their money, their financial management, and their performance during the year

Source: Acts and other documents regulating the functioning of the House of Commons.

While the Public Accounts Committee (an all-party parliamentary committee) remains the primary recipient of NAO reports, the NAO’s engagement with department select committees has grown in recent years[9]. Value for Money reports are still submitted to the Public Accounts Committee; while departmental select committees can be provided with other reports and materials, including documents that summarise audit results if the committee in question intends - or considers - discussing that topic. Using examples from its published work, the NAO outlines potential areas for performance improvement and the key issues it is likely to face in the coming year. The NAO also produces briefings and memorandums to support select committees in their scrutiny work[10].

Role of Investigations in the NAO’s Works

The NAO’s annual reports provide information on the amounts of the annual budget that are assigned to individual types of activities (National Audit Office operating segments). See Table 1.

| Budget year[11] | Audit and assurance | Value for money | Investigations and insight | Support to Parliament | International relations | Comptroller function | Voted[12] |

|---|---|---|---|---|---|---|---|

|

2014-2015 |

49,219 |

16,643 |

9,520 |

5,342 |

1,750 |

200 |

82,674 |

|

2015-2016 |

49,490 |

16,932 |

10,303 |

4,925 |

1,367 |

204 |

83,221 |

|

2016-2017 |

50,468 |

16,102 |

9,912 |

5,079 |

1,362 |

155 |

83,078 |

|

2017-2018 |

54,417 |

13,339 |

10,392 |

4,432 |

1,212 |

113 |

83,905 |

|

2018-2019 |

57,864 |

14,600 |

8,507 |

4,633 |

1,024 |

119 |

86,747 |

|

2019-2020 |

62,047 |

16,029 |

7,597 |

4,331 |

1,149 |

116 |

91,269 |

Source: NAO Annual Reports and Accounts[13].

The basic tasks of the National Audit Office are financial and value for money audits[14]. These are conducted in accordance with a separate procedure and methodology. Pre-1983 Act, VFM work was undertaken as part of financial audit work. 1983 Act provided separate powers. Increasingly in the 1990s NAO staff did either financial audit or VFM audit, but from within the same organisational unit. This is broadly the same today - each department is tracked by a joint financial audit and a VFM team, different skills and focus but working closely together.

Financial audits provide assurance that financial statements present a true and fair view, and that the money has been spent only for the purposes and in the amounts set by the parliament, as well as in compliance with the legal provisions and other regulations. It is a certification audit, similar to those carried out in the private sector but wider in scope since - apart from verifying compliance with the acts and accounting principles - the regularity of expenditure is also examined, to provide assurance that public money has been used in accordance with the relevant framework of authorities - essentially, that is consistent with legislation, regulations and government requirements. Therefore, financial audits provide information on both expenditure and income execution, and on resources utilisation. The audit procedure conforms with the principles adopted by audit firms, allowing for comparisons in the quality of work and ensures that audits are conducted in accordance with recognised standards[15]. In the budget year 2019-2020 the NAO certified 404 accounts of public bodies, including major government departments, agencies, arm’s-length bodies, companies, charities and the extensive complex commercial activities of organisations such as the BBC, Network Rail, UK Asset Resolution Ltd; 68% of the NAO’s budget was allocated to this end (in the years 2013-2020 between 53% to 68% of the budget was allocated to financial audits).

Value for money studies examine the economy, efficiency and effectiveness of individual bodies’ use of resources. Unlike the case of financial audits, where the obligation to examine accounts every year stems from legislation, here the fundamental consideration is selection of audit topics. Most often, these are in areas where the most significant resources are used, areas of public interest - both positive and negative, or where the risk to value for money is the highest. The decision on the selection of audit topics is made by the C&AG[16], taking into account the suggestions of the Public Accounts Committee. The NAO evaluates the performance of auditees and formulates suggestions and recommendations as for continuation of their practices, or as for improvements. Yet another objective of auditing is an opportunity to increase economy, efficiency or to eliminate inexpediency of their work, and to encourage the entities to apply the solutions suggested by the NAO. The Act of 1983 prohibits to question the merits of the auditees’ policy objectives. Audit topics are most often problem-oriented, e.g. management of defence capabilities[17], prevention of fraud in the social benefits system[18], water supplies management[19]. In the budget year 2019-2020, the C&AG submitted 42 value for money reports to the House of Commons; the expenditure on these accounted for 18% of the NAO’s budget (from 2013-2020, 16% to 20% of the budget).

The other main activities of the NAO include:

- investigations (to be discussed later in the article);

- cooperation with the House of Commons: in the budget year 2019-2020, the C&AG presented oral and written statements over 34 sessions of the Public Accounts Committee[20] and 15 sessions of other committees, and responded to 90 letters from MPs regarding presentation of audit results and other information; ten members of staff of the NAO were seconded to the Scrutiny Unit and select committees of the House of Commons. In order to help the Committees and individual MPs evaluate the financial management and results of ministries’ performance, the NAO elaborated eighteen departmental overviews, which are compilations of material from the previous year’s audit work on a department. In 2013-2020, some 5% to 6% of NAO’s budget was allocated for cooperation with the House of Commons;

- international relations, to which some 1% to 2% of the NAO budget was spent in 2013-2020;

- Comptroller responsibilities: the provisions of the Act of 1866[21] require the C&AG to approve the release of funds to HM Treasury and other public bodies, once he / she has satisfied himself that requests for payment are in line with relevant authorities given by Parliament[22]. In 2013-2020, some 0.1% to 0.2% of the NAO budget was allocated for this purpose.

In the NAO’s documents, value for money audits and investigations are together called major outputs, a quarter of which are reports on investigations. See Table 2.

| Financial year | Total | Value for money reports | Investigations reports |

|---|---|---|---|

|

2013-2014 |

86 |

66 |

20 (23,26%) |

|

2014-2015 |

62 |

49 |

13 (20,97%) |

|

2015-2016 |

66 |

50 |

16 (24,24%) |

|

2016-2017 |

86 |

68 |

18 (20,93%) |

|

2017-2018 |

65 |

48 |

17 (26,15%) |

|

2018-2019 |

66 |

54 |

12 (18,18%) |

|

2019-2020 |

56 |

42 |

14 (25,0%) |

Source: NAO Annual Reports and Accounts (see: footnote 13).

Description of Investigations

Concept

Until recently, the NAO mainly conducted financial and value for money audits. In 2013, the then Comptroller and Auditor General Amyas Morse introduced an additional component to address demands for timely scrutiny of specific issues of contention or debate on which NAO could provide transparency. The C&AG sought a solution that would allow the NAO, as a credible, independent and authoritative source, to report rapidly on live issues that would complement existing audit and assurance activities. As a result, investigations were introduced, and quickly became one of the NAO key activities In 2013-2020, expenditure on investigations accounted for some 8% to 15% of the budget.

The main characteristics of NAO investigations include:

- topics focused on important, live issues discussed in the media and of interest to the public;

- reactive and rapid action: the time from topic approval by the C&AG to publishing a report should not exceed three to four months;

- precise audit scopes;

- short audit reports, limited in length to approximately 5,000 words;

- fact statements without evaluations or recommendations.

Audit Topics

The National Audit Office identifies topics of investigations in the following way: ”We conduct investigations to establish the facts where there are concerns about public spending issues, such as service failures or financial irregularities. These concerns may be raised by MPs, the media or the public, or be identified through our work”[23]. Another document reads: ”Investigations allow the NAO to establish the facts when correspondence from MPs or members of the public, whistleblowers, or findings from our audit or value for money work identify concerns about the use of public funds. Investigations give a rapid and timely account of a situation or an issue”[24]. ”For example, our investigation into the circumstances surrounding the monitoring, inspection and funding of Learndirect Ltd (the UK’s largest commercial further education provider) was undertaken quickly in response to concerns reported in the media and raised by MPs”[25].

Below, for the sake of illustration, two audits (investigations) are discussed where the topics were of interest to parliament and the public:

-

Remediating dangerous cladding on high-rise buildings

On 14th June 2017, a fire broke out in the Grenfell Tower high-rise building in London. The building was constructed in the years 1972-1974, and renovated in 2015-2016, including modernisation and reinforcement of the elevation. The fire spread to all twenty-four storeys in just a quarter of an hour. 72 persons died, and 74 were injured, many reported missing. The main reason for the fire to spread so quickly was cladding made of aluminium composite material (ACM).

After this disaster, the Ministry of Housing, Communities & Local Government developed a Programme for Building Safety. In May 2018, £400 million was allocated to repairs of high-rise buildings with council flats (social housing), while in May 2019, a further £200 million was provided for renovation of private sector buildings.

The NAO investigated the supervision of the Ministry over exchange of dangerous cladding, and examined how the Ministry:

- assured that it had correctly identified the right buildings for the Programme, and that they were properly remediated;

- managed the progress of remediation;

- decided which buildings qualified for remediation funding, and made a full risk assessment.

The audit findings read: as at April 2020, 149 of a total of 456 buildings, each of 18 metres and over with unsafe ACM cladding, had been fully remediated. There are 307 buildings yet to be fully remediated, of which 167 have not yet begun remediation works. The pace of remediation has been faster in the student accommodation and social housing sectors, but slower in the private residential sector. As at April 2020, 66.7% of student accommodation blocks and 46.8% of social housing buildings had been fully remediated, compared with 13.5% of private sector residential buildings. The legal entities responsible for the private sector buildings have required more support throughout the process than initially expected. Also, not all buildings with dangerous ACM cladding fall within the scope of the government’s existing funding schemes for the social and private housing sectors. This includes high-rise hotels, student accommodation, and build-to-let blocks, as well as buildings below 18 metres. The experts have advised that the most dangerous forms of ACM cladding are unsafe on buildings of any height, and that risks are increased in buildings with elderly and vulnerable residents. The Ministry estimates there to be around 85,000 buildings in England between 11 and 18 metres, but does not know what cladding systems they have, nor whether there are any care homes under 18 metres with unsafe cladding[26].

On 6th July 2020, the Public Accounts Committee considered the NAO’s report[27]. Having interrogated representatives of the government, and listened to the opinions of associations, economic organisations and other related interested parties, on 7th September 2020, the Committee produced its report, which contained detailed firmly stated demands addressed to the Ministry[28].

-

How government increased the number of ventilators available to the NHS in response to COVID-19?

The audit found that from March 2020 the government increased the number of ventilators available to the NHS. Both the Cabinet Office and DHSC started their ventilator programmes on the basis that securing as many mechanical ventilators as possible, as quickly as possible, was necessary to safeguard public health. This urgency was reflected in their approach: getting the programmes up and running very quickly; protecting their private-sector partners from financial risk; making early commitments to contracts; paying cash upfront for ventilators before they could be inspected; showing a willingness to accept that prices were higher than the normal market rate; deliberately supporting multiple ventilator challenge options; and drawing significantly on technical expertise and capacity from the private sector. The departments spent a total of £569 million across both programmes. Inevitably, given the approach the departments took, the overall costs of both programmes are higher than would be expected in normal times. However, both departments maintained sufficient record of their programmes’ rationale, the key spending decisions they took and the information they were based on. They also put in place effective programme management, controlled costs where they could and recovered some of their committed spending once it became apparent that fewer ventilators were needed than they had originally believed[29].

On 12th October 2020, the Public Accounts Committee considered the NAO’s report and questioned the representatives of the Cabinet Office and DHSC. The Committee’s report was approved on 18th November 2020[30].

Below there are several further examples of investigation topics:

- lack of transparency, consistency and accountability in special severance payments and confidentiality clauses in the public sector[31];

- government travel expenditure[32];

- employers’ compliance with minimum wage regulations[33];

- high spending on generic medicines in primary care[34];

- health screening[35];

- transferring government’s funds to self-government administration bodies[36];

- defueling and dismantling of nuclear submarines withdrawn from use[37];

- overpayments of carer’s allowance[38];

- response to cheating in English language tests related to visa granting[39];

- Departments’ use of consultants to support preparations for EU Exit[40];

- military flying training[41];

- pre-school vaccinations[42];

- impact of Carillion’s bankruptcy [largest bankruptcy of a construction company in the history of the UK] on hospital contracts[43];

- government’s response to the collapse of Thomas Cook travel agency[44].

The National Audit Office has already published over a hundred investigation audit reports. They provide a dynamic and colourful illustration of public life, with the public’s most important concerns being addressed. In general, the topics of investigation are related to situations with which the MPs, citizens, whistleblowers, media, etc. have issues or suspect that things do not work as they should, or when problems exist that - regardless of the reason - should be solved by government, or at least call for government opinion. For example:

- government programme implementation, effectiveness and quality of management, e.g. measured against their failure to achieve the expected results or changes of the programme;

- government’s (competent department’s) activities in response to emerging or unexpected issues that raise concerns of the public (epidemics, catastrophes, bankruptcies of companies of high importance to the economy, etc.);

- problems with accessing public services;

- compliance with the law, especially in the areas of high importance to citizens or private entities;

- distribution of government resources (e.g. subsidies), often in the context of alleged privileges;

- other problems with transparency and accountability of the administration, including conflicts of interests.

Therefore, like VFM studies, the main addressees of investigations are not only state bodies (parliament, government, etc.), but also - and sometimes in the first place - the citizens.

Audit Process

The audit process of investigations closely follows the VFM process, comprising:

- initial proposal;

- scope of examination and schedule of works; approval of the planning document by the C&AG;

- fieldwork and first draft report development;

- evaluation of the report within the NAO, potential modifications;

- report approval by the C&AG;

- clearance procedure with the auditee (confirmation of factual accuracy);

- report published and laid in the House of Commons;

- follow up.

The initial proposals for topics are formulated during a planning meetings between NAO teams with responsibility for the audit of specific government departments (e.g. Defence, Health etc.), the Central Investigations Team and also teams responsible for parliament and media relations. The results of these planning meetings are presented to the C&AG periodically. The NAO decides on if an investigation is the best approach through considering whether: a facts-only only investigation will add value, the scope is suitably narrow, the amount of work planned is realistic within the timeframe. Then the audit team (or the Central Investigations Team, e.g. when the audit topic exceeds the competence of one ministry) develops a document on the audit concept and plan, to be approved by the C&AG. It needs to be emphasised that the Budget Responsibility and National Audit Act 2011 (Part 2) sets out that, within specified parameters, the C&AG has complete discretion as to the work programme and how it is executed.

The key issue is to select a topic that will add value to accountability and transparency over the use of public funds, and that more timely reporting will help government learn lessons and drive improvements. A good example of this is the NAO’s use of investigations in auditing the response to the COVID-19 pandemic - producing several reports, heard by the PAC, which have already informed changes to the government’s response. This means that the topic has to be more suited to being developed quickly (e.g. the scope has to be defined tightly and be suitable for examination) - so that the audit report can be ready within three-four months since the approval of the topic by the C&AG, although this is not always feasible. If the initial analysis of the topic shows that the area under consideration is more complex, the VFM risks are great and that a report in 6-9 months would not add to the VFM risk, or that data collection requires more time, a decision can be taken to conduct a full value for money study in the area. This is related to another criterion: how precise the topic is so that it can be presented briefly: reports are expected to be no more than 5,000 words (VFM target is 10,000); in practice the average length is 6,700 words, although some reports are below 5,000 words.

After the topic has been approved, data is collected and an initial draft worked on. Work is done in accordance with the value for money methodology, with some differences. The basic difference is that - unlike financial and value for money audits - reports on investigations do not typically contain evaluations or recommendations[45]. This saves time (to develop evaluations and recommendations is time consuming, and additional time is needed for discussions with the auditee), but there are other reasons for this, too: the facts often speak for themselves. The objective is to present the text in a way that allows the readers to draw their own conclusions.

The differences also stem from the nature and scope of the topic: investigations are more reactive to external events, they put greater focus on increasing accountability and transparency, contain narrower issues (less complex than value for money issues), rely on a flexible and agile workforce. Investigations are usually two or three times quicker than value for money studies[46]. Despite the short time for their development, reports on investigations have to meet strict audit quality requirements, as in the case of other NAO reports, e.g. the draft report is evaluated by a Case Manager from Central Investigations Team and the Partner Director (internal peer review)[47].

Like NAO VFM studies, an interesting element of the procedure is the draft report summary that is used in the internal quality procedure, and later submitted to the Comptroller and Auditor General to test its logic, and from an accountability perspective to demonstrate the audit team is delivering on the scope approved by the C&AG earlier in the process. It also tests whether the report presents facts without evaluation: are the logic and presentation of the facts set out in a manner which will encourage people to come to conclusions and will a facts-only investigation achieve the desired outcome.

The final draft report is submitted to the department’s Permanent Secretary (highest civil service official) who confirms the facts or gives comments[48]. Actually, it is the crowning stage of confirmation, since the facts have been already established at the working level at earlier stages.

Once the report is signed, it is submitted to the House of Commons and published on the NAO website, however not all investigations need to be laid before parliament if the same, or a different impact, can be achieved. Some reports are published on the NAO website without being submitted to parliament, or full reports are not written and instead a Management Letter is sent to the competent administration body instead. The decision on how to proceed depends on the importance of the findings, as well as the assumption that the chosen path will ensure the best impact possible.

Although investigations are usually well received by the Public Accounts Committee (that sometimes provides inspiration for investigations), like VFM reports not all investigation reports are discussed by the Committee. This is mainly due to the lack of time: the NAO submits 50-60 value for money reports annually, the majority of which are considered by the Committee. There are also two-three sessions to discuss financial audit reports; moreover the Committee, on its own initiative, selects several other topics on which the NAO may deliver information. Traditionally, the Committee meets two times a week; if holidays and other breaks are excluded, this would mean some 50-60 meetings annually. More or less every four months, the Committee considers the work plan for the next period - which gives an opportunity for deciding which investigation reports can be discussed.

Directly before publication of a report, the NAO issues a press release to the media, which includes a summary of the key points and can choose to answer questions. The investigations receive good media coverage perhaps because they are released at a time when public and media interest in a topic is still high.

Are Investigations a Type of Audit?

In Polish doctrine, ”an audit relies on examination and evaluation of a given activity or state”. It comprises:

- providing an actual illustration of the given activity or situation at the given moment;

- evaluation of this activity or situation, leading to a statement of whether these are correct or not;

- indicating the reasons for potential irregularities;

- providing conclusions on how to prevent irregularities in future[49].

The International Standards of Supreme Audit Institutions (ISSAIs) perceive auditing in a similar way: ”In general public-sector auditing can be described as a systematic process of objectively obtaining and evaluating evidence to determine whether information or actual conditions conform to established criteria. Public sector auditing is essential in that it provides legislative and oversight bodies, those charged with governance and the general public with information and independent and objective assessments concerning the stewardship and performance of government policies, programmes or operations”[50].

Therefore a question arises as to whether the NAO’s investigations are audits. In the light of the definitions referred to above, the answer should be ”No”, however it is worthwhile looking at the case in a broader context:

- investigation reports usually do not contain evaluations or recommendations, however they present information in a way that enables the reader to form their own judgements on the stewardship of public funds[51]. Audit conclusion can sometimes be read between the lines. For example, if in a report the question is asked ”was the item more expensive than expected?”, facts will be presented as a response, but in my view actually the answer will amount to an evaluation, too.

- Investigations are related to other NAO audits: financial and value for money, as well as compliance (legality) audits, which are their element. Investigation topics are often inspired by topics from other NAO audits, too. Indeed, investigation reports do not comprise evaluations or recommendations, yet they are conducted in accordance with the value for money methodology and in pursuance of the same statutory powers as value for money examinations;

- The most important argument is that audit recommendations do not have to be present in audit reports in order to be implemented - and they can be implemented through other mechanisms, such as evaluations and recommendations of parliamentary committees or pressure of the media. This is particularly the case in the British system: if the PAC decides to hold a hearing, produces its own report detailing the results of the hearing, referencing the NAO’s report. The PAC report contains recommendations to Government, who have to provide a formal response known as a Treasury Minute. This is the same for both VFM and investigations.

The above arguments allow for treating investigations as a new type of audit, similar to performance audit, with the main difference relying on a distinct (more dispersed) form of development and implementation of evaluations and recommendations. The issue is however still debatable.

Final Remarks

The National Audit Office of the United Kingdom has developed and introduced a new type of audit which complements - rather than replaces - the public sector audit practice to date. These new audits - called investigations, although they have nothing to do with criminal investigations - rely on the selection of topics related to important, current issues, discussed in the media, and of special interest to the public; they take less time to conduct than other audits; they have a specific and rather narrow scope; reports on their findings are brief and accessible, and contain only information on facts, without evaluations or recommendations. Investigations have helped the NAO to remain relevant in the challenging and changing environment, contribute to ”live” issues that concern its stakeholders, and also bring to the fore its expertise and knowledge. They have enabled the NAO to respond quickly and provide transparency over the UK government’s response to the COVID-19 pandemic in a timelier way than other audit approaches would have[52].

An additional relevant factor is the development of technology used to transfer and provide information (e.g. the internet), which affects the contact between state bodies and citizens, as well as social behaviour (e.g. social media). Simultaneously, since investigations deal with concerns of interest to MPs, citizens, whistleblowers, or the media - expressing fears or suspecting irregularities or problems that - regardless of their reason - call for government intervention or, at least, government opinion - apart from state bodies (parliament, government, etc.), investigations help citizens become more engaged with the NAO’s work[53]. The international guidance on public audit state that - when selecting audit topics - SAIs should consider emerging risks and respond to them accordingly; they should deal with current issues that are debated by citizens and are of concern to the citizens’[54]. It is not enough to deal with what happened in the past - issues that are important today need to be reviewed.

The National Audit Office has already conducted over a hundred investigations, and for several years investigations have been a large part of its activities. The Supreme Audit Institutions of other countries (e.g. Denmark, Latvia, the Netherlands, Poland, Slovakia, Sweden) and the European Court of Auditors have also introduced new solutions to respond fast to important and topical issues; these will be discussed in another article. There are both benefits and risks inherent in such changes, so they have to be properly prepared, taking into account the legal basis and political system of a given country, as well as the experience, tradition and capacity of the relevant Supreme Audit Institution.

JACEK MAZUR, Ph.D.

Advisor to the President of the Polish Supreme Audit Office (NIK)

Key words: investigations, performance audit, UK National Audit Office, SAI of the United Kingdom, NAO

The views expressed in this article are personal, and should not be attributed to the institutions the author is employed in.

[1] More on the British accountability system in: Managing public money, HM Treasury, July 2013 with annexes, revised as at September 2019: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/835558/Managing_Public_Money__MPM__with_annexes_2019.pdf (accessed 17.10.2020).

[2] National Audit Act 1983 (hereinafter referred to as the Act of 1983); https://www.legislation.gov.uk/ukpga/1983/44/contents/enacted (accessed 1.10.2020). For the British state audit system see: R. Szawłowski: Kontrola państwowa w Wielkiej Brytanii (National Audit in the United Kingdom), ”Kontrola Państwowa” No. 2/1957; State Audit in the European Union, UK National Audit Office, London 2005, pp. 260-269; D. Dewar, W. Funnell: A History of British National Audit: The Pursuit of Accountability, Oxford 2017.

[3] J. Mazur: Kontroler i Audytor Generalny Wielkiej Brytanii (Comptroller and Auditor General of the United Kingdom), ”Kontrola Państwowa” No. 1/1995. For specific aspects of the activity of the National Audit Office see: J. Kobeszko: Kontrola finansowa realizowana przez Narodowy Urząd Kontroli Wielkiej Brytanii (Financial Audit of the National Audit Office of the United Kingdom), ”Kontrola Państwowa” No. 4/1995; T. Bolek, M. Góra: Narodowy Urząd Kontroli Wielkiej Brytanii - niektóre aspekty działalności kontrolnej i organizacji (National Audit Office of the United Kingdom - Selected Aspects of the Audit Activity and Organisation), ”Kontrola Państwowa” No. 2/1996; J. Owczarek: Value for money, czyli efekt za pieniądze (Value for Money, or What we Pay for) ”Kontrola Państwowa” No. 3/1997; J. Ashcroft: Mierzenie efektów działalności Narodowego Urzędu Kontroli Wielkiej Brytanii (Measuring the Effects of the Activity of the National Audit Office of the United Kingdom), ”Kontrola Państwowa” No. 6/1998; M. Pomianowska, S. Grzelak: Działalność informacyjna Narodowego Urzędu Kontroli Wlk. Brytanii (Information Activity of the National Audit Office of the United Kingdom), ”Kontrola Państwowa” No. 6/1999; W. Zdasień: Kontrola „efekt za pieniądze” - value for money na przykładzie dorobku Narodowego Urzędu Kontroli Wielkiej Brytanii (Value for Money Audits on the Basis of the Achievements of the National Audit Office of the United Kingdom), ”Kontrola Państwowa” No. 2/2001; J. Mazur: Poszukiwanie wymiernych wskaźników oceny w kontroli wykonania budżetu państwa (Doświadczenia Wielkiej Brytanii, Stanów Zjednoczonych i Portugalii) (Searching for Measurable Indicators to Evaluate State Budget Execution (Experience of the United Kingdom, the United States and Portugal)), ”Kontrola Państwowa” No. 6/2000; J. Mazur: Audyt wykonania budżetu państwa przez najwyższe organy kontroli w niektórych krajach (State Budget Execution Audit by Supreme Audit Institutions in Several States), ”Kontrola Państwowa” No. 4/2002; J. Mazur: Kontrola jakości postępowania kontrolnego w Narodowym Urzędzie Kontroli Wielkiej Brytanii (w zakresie kontroli finansowej) (Quality Control of the Audit Process in the National Audit Office of the United Kingdom (with Regard to Financial Audit)), ”Kontrola Państwowa” No. 5/2003. For brief, synthetic information on the National Audit Office see the publication of the European Court of Auditors, elaborated jointly with the Supreme Audit Institutions of the EU Member States: Public Audit in the European Union, European Court of Auditors, Luxembourg 2019, pp. 216-224; https://www.eca.europa.eu/Lists/ECADocuments/Book_Public_Audit_in_the_EU/Book-Public_Audit_in_the_EU_EN.pdf (accessed 2.10.2020).

[4] Budget Responsibility and National Audit Act 2011 (hereinafter referred to as the Act of 2011); https://obr.uk/docs/dlm_uploads/Budget-Responsibility-and-National-Audit-Act-2011.pdf (accessed 8.08.2020).

[5] In the Act of 2011, the NAO Board is referred to as ”National Audit Office”. In practice, the body is usually called ”the Board”, while the term ”National Audit Office” refers to staff (see: the website of the National Audit Office: https://www.nao.org.uk/about-us/our-work/governance-of-the-nao/nao-board; accessed 1.10.2020); see also: Public Audit…, ibid, pp. 218-220. Although the NAO Board and the Comptroller and Auditor General are public bodies, in the literature and media the UK Supreme Audit Institution started being called the ”National Audit Office”; this terminology is also used in this article.

[6] The introduction in 2011 of close supervision of the C&AG’s activity (apart from audit-related work) was due to the criticism of the activities of Sir John Bourn (Comptroller and Auditor General in the years 1988-2008), who was accused of, inter alia, spending too much of his working time in costly - and not always necessary - foreign trips. See e.g.: A. Whittam Smith: Who guards Britain’s auditing guardian? If Sir John Bourn wishes to travel a lot, he should retire and do it in his own time, ”The Independent”, 14 May 2007; G. Hurst: ‚Spendthrift’ public spending watchdog to retire, ”The Times”, 26 October, 2007; T. Branigan: Big-spending cost watchdog to retire. Massive travel and meal bills drew criticism. Decision ‚not connected to expenses row’; ”The Guardian”, 26 October 2007. On the basis of this information, the Public Accounts Commission examined the NAO’s management and suggested changes; Corporate Governance of the National Audit Office: Response to John Tiner’s Review, The Public Accounts Commission, 4 March 2008, HC402; https://publications.parliament.uk/pa/cm200708/cmselect/cmpacomm/402/402.pdf (accessed 11.10.2020).

[7] https://www.nao.org.uk/about-us/our-work/governance-of-the-nao/ (accessed 11.11.2020).

[8] The Public Accounts Commission is a body of the House of Commons established on the basis of the Act of 1983 to consider the draft budget and assess budget achievement of the National Audit Office; following the Act of 2011, the Commission’s role has expanded. Membership of the Public Accounts Commission includes the Chair of the Public Accounts Committee, the Leader of the House of Commons - the leader of the governmental majority in the House of Commons (simultaneously the minister responsible for the organisation of the House’s work and cooperation between the government and the House of Commons), and seven backbench MPs.

[9] J. Mazur: Kontroler…, ibid, pp. 162-163; H. Pajdała: Komisje w parlamencie współczesnym (Committees in the Contemporary Parliament), Warszawa 2001, pp. 87-93; A.S. Bidwell: Reformowanie procedur Izby Gmin parlamentu brytyjskiego w XXI wieku (Reforming procedures of the House of Commons of the British Parliament in the 21st century), ”Przegląd Sejmowy” No. 3/2012; R. Kelly: Select Committees core tasks, House of Commons Library, Briefing Paper No. 3161, 2 April 2020.

[10] For instance The Third Sector and Public Policy - Options for Committee Scrutiny, 12 October 2006 (publication for the Public Administration Committee); Performance Brief: A summary of National Audit Office Reports of the Department for Transport 2007-08, 18 January 2008 (information for the Transport Committee); Renewable energy: Options for scrutiny, 1 July 2008 (publication for the Environmental Audit Committee); The work of the Department for International Development in 2009-10 and its priorities for reform, 2 December 2010 (publication for the International Development Committee); Briefing for the Women and Equalities Committee: The Equality and Human Rights Commission, 12 January 2017 (publication for the Equality and Human Rights Commission).

[11] From 1st April to 31st March.

[12] The amounts do not comprise the remuneration of the Comptroller and Auditor General or the Chair of the NAO Board since these are paid from the Consolidated Fund, and not from the NAO budget

[13] Annual Report and Accounts 2013-14, UK National Audit Office, 9 June 2014, p. 85, https://www.nao.org.uk/wp-content/uploads/2014/06/NAO-annual-report-2013-141.pdf (accessed 11.07.2020); Annual Report and Accounts 2014-15, UK National Audit Office, 16 June 2015, p. 88, https://www.nao.org.uk/wp-content/uploads/2015/06/nao-annual-report-2014-15.pdf (accessed 11.07.2020); Annual Report and Accounts 2015-16, UK National Audit Office, 29 June 2016, p. 108, https://www.nao.org.uk/wp-content/uploads/2016/06/NAO-Annual-Report-2015-16.pdf (accessed 11.07.2020); Annual Report and Accounts 2016-17, UK National Audit Office, 23 June 2017, p. 106, https://www.nao.org.uk/wp-content/uploads/2017/06/NAO-Annual-Report-and-Accounts-2016-17.pdf (accessed 11.07.2020); Annual Report and Accounts 2017-18, UK National Audit Office, 26 June 2018, p. 104, https://www.nao.org.uk/wp-content/uploads/2018/06/NAO-Annual-Report-and-Accounts-2017-18.pdf (accessed 11.07.2020); Annual Report and Accounts 2018-19, UK National Audit Office, 6 June 2019, p. 99, https://www.nao.org.uk/wp-content/uploads/2019/06/NAO-Annual-Report-and-Accounts-2018-19.pdf (accessed 11.07.2020); Annual Report and Accounts 2019-20, UK National Audit Office, 23 June 2020, p. 127, https://www.nao.org.uk/wp-content/uploads/2020/06/nao-annual-report-accounts-2019-20.pdf (accessed 11.07.2020).

[14] The NAO does not conduct separate compliance (legality) audits. The assessment of whether the audited activity is compliant with legal norms is made within financial and value for money audits.

[15] J. Mazur: Audyt…, ibidem, ”Kontrola Państwowa” No. 4/2002 and the literature referred to therein.

[16] See https://www.nao.org.uk/about-us/wp-content/uploads/sites/12/2016/10/The-Comptroller-and-Auditor-General-powers.pdf.

[17] This study examined whether the Ministry of Defence (the Department) has the capability to meet its current and future defence objectives when it needs them. The intention was to evaluate defence capabilities provision from the beginning of the delivery process and setting requirements by the Ministry, until the achievement of operational capabilities. The NAO examined the extent and causes of delays and shortfalls in bringing capabilities into service, the completeness of the Department’s system for monitoring the delivery of capabilities and whether the Department was putting in place appropriate arrangements to transform its capability delivery in the future. Defence capabilities - delivering what was promised, UK National Audit Office, 18 March 2020; https://www.nao.org.uk/wp-content/uploads/2020/03/Defence-capabilities-delivering-what-was-promised.pdf (accessed 4.10.2020).

[18] The Department for Work and Pensions introduced a system to replace the former six benefits for persons of economically productive age (Universal Credit). The benefits are settled and paid at the end of the payment period, hence beneficiaries have to wait for payment for at least five weeks after applying; simultaneously the Department allowed for transfer of advance payments on the basis of an estimate of the first payment. When the system was launched, the media focused on potential fraud, e.g. providing fake data to increase the advances, or using the data of other persons. The objective of the audit was to evaluate how the Department dealt with fraud and whether this had been included in risk assessment, what actions had been taken to prevent fraud, and what could be done to reduce fraud in the future. Universal Credit advances fraud, UK National Audit Office, 20 March 2020; https://www.nao.org.uk/wp-content/uploads/2020/03/Universal-Credit-advances-fraud.pdf (accessed 4.10.2020).

[19] The audit of the effectiveness of the supervision of the Department for Environment, Food & Rural Affairs; how the Department provided guidance to regulators and companies to ensure long-term water supplies: Water supply and demand management, UK National Audit Office, 25 March 2020; https://www.nao.org.uk/wp-content/uploads/2020/03/Water-supply-and-demand-management.pdf (accessed 4.10.2020).

[20] In relation to the parliamentary elections (December 2019) the number was lower than usual since the Committee did not meet at the end of 2019 or at the beginning of 2020. For comparison, in the budget year 2018-2019, the C&AG participated in 61 sessions of the Public Accounts Committee.

[21] Exchequer and Audit Department Act 1866.

[22] The audit type was discussed by R. Szawłowski, ibidem, pp. 24-25.

[23] Annual Report and Accounts 2019-20, ibidem, p. 24.

[24] Annual Report and Accounts 2018-19, ibidem, p. 7.

[25] Annual Report and Accounts 2017-18, ibidem, p. 27.

[26] Investigation into remediating dangerous cladding on high-rise buildings, UK National Audit Office, 19 June 2020; https://www.nao.org.uk/wp-content/uploads/2020/06/Investigation-into-remediating-dangerous-cladding-on-high-rise-buildings.pdf (accessed 11.10.2020).

[27] House of Commons, Public Accounts Committee; Oral evidence: Progress in Remediating Dangerous Cladding, HC 406, Monday 6 July 2020; https://committees.parliament.uk/oralevidence/639/pdf/ (accessed 15.10.2020).

[28] House of Commons, Public Accounts Committee; Progress in remediating dangerous cladding, Sixteenth Report of Session 2019-21; 7 September 2020; https://committees.parliament.uk/publications/2561/documents/25986/default/ (accessed 15.10.2020).

[29] Investigation into how government increased the number of ventilators available to the NHS in response to COVID-19, UK National Audit Office, 30 September 2020; https://www.nao.org.uk/wp-content/uploads/2020/09/Investigation-into-how-the-Government-increased-the-number-of-ventilators.pdf (accessed 11.10.2020).

[30] House of Commons, Public Accounts Committee; Oral evidence: COVID-19: Supply of ventilators, HC 685, Monday 12 October 2020; https://committees.parliament.uk/oralevidence/1033/default/ (accessed 15.10.2020). House of Commons, Public Accounts Committee; Covid-19: Supply of ventilators, Twenty-Seventh Report of Session 2019-21; 7 September 2020; https://committees.parliament.uk/publications/3639/documents/35370/default/ (accessed 9.12.2020).

[31] Confidentiality clauses and special severance payments, UK National Audit Office, 21 June 2013; https://www.nao.org.uk/wp-content/uploads/2013/06/10168-001-Confidentiality-clauses-and-payments1.pdf (accessed 17.10.2020).

[32] Investigation into government travel expenditure, UK National Audit Office, 11 March 2015; https://www.nao.org.uk/wp-content/uploads/2015/03/Investigation-into-government-travel-expenditure.pdf (accessed 15.10.2020).

[33] Ensuring employers comply with National Minimum Wage regulations, UK National Audit Office, 11 May 2016; https://www.nao.org.uk/wp-content/uploads/2016/05/Ensuring-employers-comply-National-Minimum-Wage-regulations.pdf (accessed 17.10.2020).

[34] Investigation into NHS spending on generic medicines in primary care, UK National Audit Office, 8 June 2018; https://www.nao.org.uk/wp-content/uploads/2018/06/Investigation-into-NHS-spending-on-generic-medicines-in-primary-care.pdf (accessed 17.10.2020).

[35] Investigation into the management of health screening, UK National Audit Office, 1 February 2019; https://www.nao.org.uk/wp-content/uploads/2019/01/Investigation-into-the-management-of-health-screening.pdf (accessed 16.10.2020).

[36] Investigation into devolved funding, UK National Audit Office, 13 March 2019; https://www.nao.org.uk/wp-content/uploads/2019/02/Investigation-into-devolved-funding.pdf (accessed 17.10.2020).

[37] Investigation into submarine defueling and dismantling, UK National Audit Office, 3 April 2019; https://www.nao.org.uk/wp-content/uploads/2019/04/Investigation-into-submarine-defueling-and-dismantling.pdf (accessed 17.10.2020).

[38] Investigation into overpayments of Carer’s Allowance, UK National Audit Office, 26 April 2019; https://www.nao.org.uk/wp-content/uploads/2019/04/Investigation-into-overpayments-of-Carers-Allowance.pdf (accessed 15.10.2020).

[39] Investigation into the response to cheating in English language tests, UK National Audit Office, 24 May 2019; https://www.nao.org.uk/wp-content/uploads/2019/05/Investigation-into-the-response-to-cheating-in-English-language-tests.pdf (accessed 15.10.2020).

[40] Departments’ use of consultants to support preparations for EU Exit, UK National Audit Office, 7 June 2019; https://www.nao.org.uk/wp-content/uploads/2019/05/Departments-use-of-consultants-to-support-preparations-for-EU-Exit.pdf (accessed 16.10.2020).

[41] Investigation into military flying training, UK National Audit Office, 4 September 2019; https://www.nao.org.uk/wp-content/uploads/2019/09/Investigation-into-Military-flying-training.pdf (accessed 16.10.2020).

[42] Investigation into pre-school vaccinations, UK National Audit Office, 25 October 2019; https://www.nao.org.uk/wp-content/uploads/2019/08/Investigation-into-pre-school-vaccinations.pdf (accessed 15.10.2020).

[43] Investigation into the rescue of Carillion’s PFI hospital contracts, UK National Audit Office, 17 January 2020; https://www.nao.org.uk/wp-content/uploads/2020/01/Investigation-into-the-rescue-of-Carillions-PFI-hospital-contracts.pdf (accessed 16.10.2020).

[44] Investigation into government’s response to the collapse of Thomas Cook, UK National Audit Office, 19 March 2020; https://www.nao.org.uk/wp-content/uploads/2020/03/Investigation-into-governments-response-to-the-collapse-of-Thomas-Cook.pdf (accessed 16.10.2020).

[45] Some investigations reports, exceptionally, contain evaluations, e.g. the report on ventilators purchase referred to above.

[46] In the budget year 2014-2015, the average value for money audit lasted over nine months; Annual Report and Accounts 2014-15, p. 22 (see: footnote 15).

[47] Data on the investigation process come from the presentation delivered by the NAO’s representatives at the EUROSAI Seminar held on 14-15 November 2018 in London (see: News (Strategic Goal 1): Output of ”Investigations” seminar published; https://www.eurosai.org/en/calendar-and-news/news/News-Strategic-Goal-1-Output-of-Investigations-seminar-published-00001/; accessed 18.10.2020) and at the online EUROSAI Seminar organised on 16 July 2020 by the SAI of the Netherlands. See also: L. Summerfield: NAO Investigates, 7 July 2017; https://www.nao.org.uk/naoblog/nao-investigates/#more-1832 (accessed 18.10.2020).

[48] This is the usual clearance process as is in place for VFM reports. The audited body is asked to confirm the accuracy of the facts and the fairness of the presentation. It is not a case of the senior civil servant giving approval. In some cases they may disagree with the facts but the C&AG may still publish.

[49] J. Jagielski: Kontrola administracji publicznej (Public Administration Auditing), Warszawa 2006, pp. 11-18; L. Kurowski, E. Ruśkowski, H. Sochacka-Krysiak: Kontrola finansowa w sektorze publicznym (Financial Audit in the Public Sector), Warszawa 2000, pp. 14-20; Z. Dobrowolski: Teoretyczne podstawy kontroli (Theoretical Foundations of Auditing), Zielona Góra 2003, pp. 9-12. The same definition of auditing has been adopted in Glossary of Terms Related to Audit in Public Administration, Warszawa 2005, p. 32; https://www.nik.gov.pl/plik/id,3364.pdf (accessed 13.11.2020).

[50] ISSAI 100 Fundamental Principles of Public-Sector Auditing, INTOSAI, 2019; https://www.issai.org/wp-content/uploads/2019/08/ISSAI-100-Fundamental-Principles-of-Public-Sector-Auditing.pdf (accessed 11 May 2020).

[51] NAO Strategy 2019-20 to 2021-22, UK National Audit Office, December 2018, p. 16; https://www.nao.org.uk/wp-content/uploads/2019/02/NAO-Strategy-2019-20-to-2021-22.pdf (accessed 12.07.2020).

[52] https://www.nao.org.uk/covid-19/

[53] More and more Supreme Audit Institutions regard the citizens as their main stakeholders, next to parliaments and governments; J. Mazur: New Trends in the Works of Supreme Audit Institutions, ”Kontrola Państwowa” No. 3/2020.

[54] INTOSAI P-12 The Value and Benefits of Supreme Audit Institutions - making a difference to the lives of citizens, 2019, p. 10; https://www.issai.org/pronouncements/intosai-p-12-the-value-and-benefits-of-supreme-audit-institutions-making-a-difference-to-the-lives-of-citizens/ (accessed 10.10.2020)

Selected bibliography

- Annual Report and Accounts 2019-20, National Audit Office, 23 June 2020.

- D. Dewar: The Audit of Central Government, in: Current Issues in Auditing, ed. by M. Sherer and S. Turley, London 1991.

- D. Dewar, W. Funnell: A History of British National Audit: The Pursuit of Accountability, Oxford 2017.

- ISSAI 100 Fundamental Principles of Public-Sector Auditing, INTOSAI, 2019.

- Glossary of Terms Related to Audit in Public Administration, Warszawa 2005.

- J. Jagielski: Kontrola administracji publicznej (Public Administration Auditing), Warszawa 2006.

- R. Kelly: Select Committees core tasks, House of Commons Library, Briefing Paper No 3161, 2 April 2020.

- Public Audit in the European Union, European Court of Auditors, Luxembourg 2019.

- Managing public money, HM Treasury, July 2013 with annexes revised as at September 2019.

- J. Mazur: Kontroler i Audytor Generalny Wielkiej Brytanii (Comptroller and Auditor General of the United Kingdom), „Kontrola Państwowa” nr 1/1995.

- J. Mazur: Audyt wykonania budżetu państwa przez najwyższe organy kontroli w niektórych krajach (State Budget Execution Audit by Supreme Audit Institutions in Several States), „Kontrola Państwowa” nr 4/2002.

- J. Mazur: Kontrola jakości postępowania kontrolnego w Narodowym Urzędzie Kontroli Wielkiej Brytanii (w zakresie kontroli finansowej) (Quality Control of the Audit Process in the National Audit Office of the United Kingdom (with Regard to Financial Audit)), „Kontrola Państwowa” nr 5/2003.

- J. Mazur: New Trends in the Works of Supreme Audit Institutions, „Kontrola Państwowa” Nr 3/2020.

- J. Owczarek: Value for money, czyli efekt za pieniądze (Value for Money, or What we Pay for), „Kontrola Państwowa” nr 3/1997.

- H. Pajdała: Komisje w parlamencie współczesnym (Committees in the Contemporary Parliament), Warszawa 2001.

- L. Summerfield: NAO Investigates, 7 July 2017; https://www.nao.org.uk/naoblog/nao-investigates/#more-1832>.

- State Audit in the European Union, UK National Audit Office, London 2005.

- R. Szawłowski: Kontrola państwowa w Wielkiej Brytanii (National Audit in the United Kingdom), „Kontrola Państwowa” nr 2/1957.