The National Revenue Administration (Krajowa Administracja Skarbowa, KAS) has not always conducted preliminary proceedings in criminal tax cases correctly and thoroughly. The irregularities mainly concerned delays in initiating proceedings and in applying for extensions to the deadlines for their conclusion. The reorganisation of the criminal tax units (SKK units) was intended to enable the effective management of human resources, address disparities in workload and ensure the continuity of operations in the face of staffing challenges, and thereby streamline proceedings and improve the quality of services provided by the designated offices. During the period covered by the NIK audit (2022–2024), efforts continued to optimise the functioning of the criminal tax units in the designated offices. However, NIK’s findings indicate that, following the introduction of the changes, some of the statistics relating to criminal tax proceedings did not improve – in the first two years following the reorganisation, the number of preliminary proceedings initiated and concluded fell compared with the two preceding years. According to NIK, this requires further monitoring and analysis of the effects of the reorganisation by the Ministry of Finance.

Changes to tax offices came into effect on 1 January 2023. The new organisation was intended to facilitate the conduct of preliminary proceedings in criminal tax cases. The number of tax offices conducting preliminary proceedings has been reduced from 400 to 16 – one for each voivodship. In those offices whose heads have been appointed to conduct preliminary proceedings and represent the authorities in court in cases involving fiscal offences and misdemeanours, fiscal criminal divisions have been established, comprising fiscal criminal units.

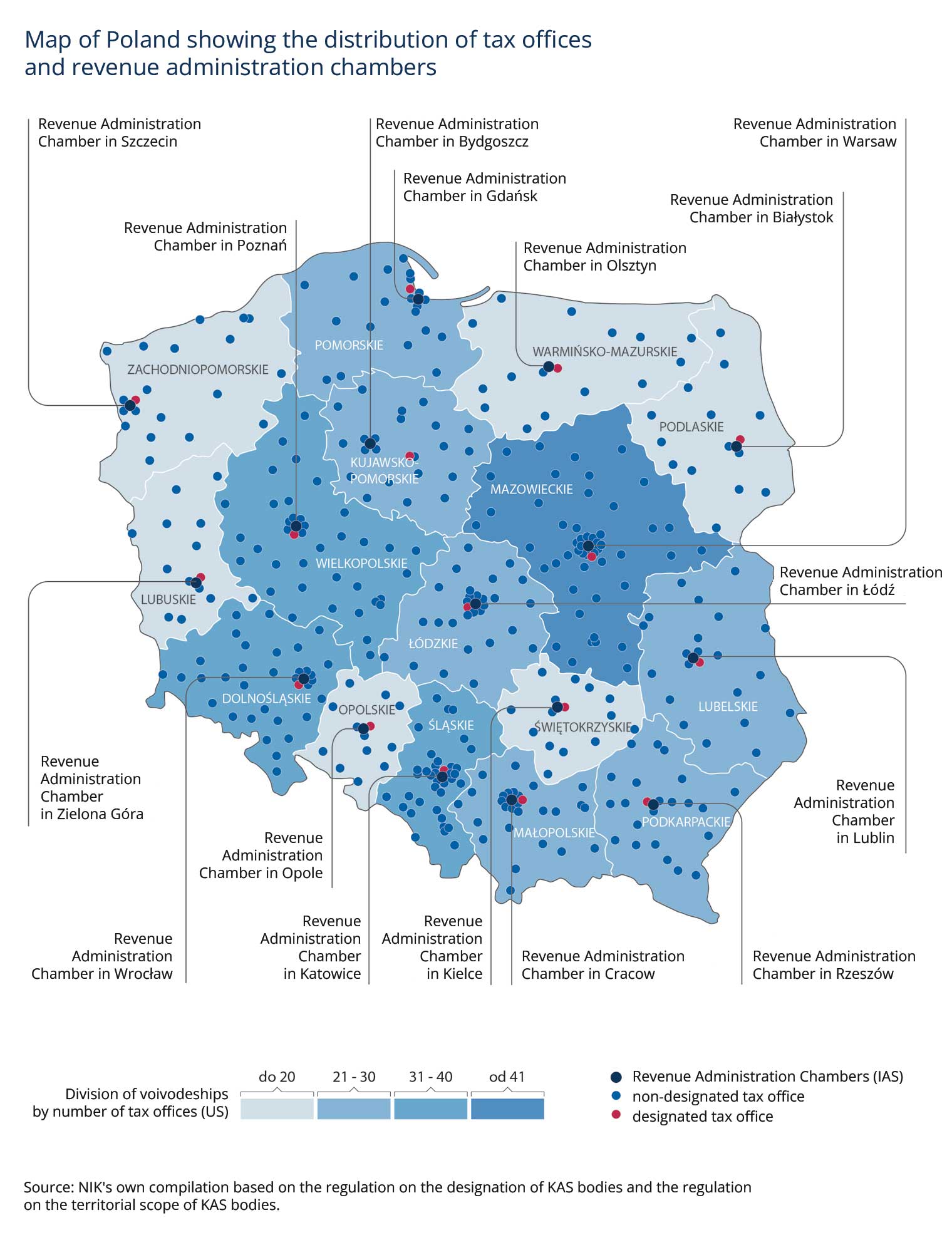

Description of the image

Map of Poland showing the distribution of tax offices and revenue administration chambers

- Revenue Administration Chambers (IAS): located in the following cities: Szczecin, Poznań, Zielona Góra, Wrocław, Opole, Katowice, Bydgoszcz, Gdańsk, Olsztyn, Warsaw, Białystok, Łódź, Kielce, Kraków, Rzeszów, Lublin.

-

Division of voivodeships by number of tax offices (US):

- Up to 20 offices: Lubuskie, Opolskie, Świętokrzyskie, Podlaskie, Warmińsko-mazurskie.

- 21 – 30 offices: Zachodniopomorskie, Pomorskie, Kujawsko-pomorskie, Łódzkie, Lubelskie, Podkarpackie.

- 31 – 40 offices: Dolnośląskie, Małopolskie.

- Over 41 offices: Wielkopolskie, Mazowieckie, Śląskie.

-

Point Legend:

- Dark blue dots: revenue administration chamber.

- Light blue dots: non-designated tax office.

- Pink dots: designated tax office.

Source: NIK's own compilation based on the regulation on the designation of KAS bodies and the regulation on the territorial scope of KAS bodies.

The reorganisation was intended to enable effective staff management and to even out the uneven workload between offices within a given revenue administration chamber. It was also intended to facilitate the exchange of experiences among staff within the new multi-member fiscal criminal affairs units and to ensure the continuity of operations in the event of staff absences. As a result, the organisational changes were intended to have a positive impact on the quality and efficiency of the tasks carried out and to improve the operational efficiency of the revenue administration without altering its resources.

The audit covered the years 2022–2024 and was the first to examine the issue of preliminary proceedings in criminal tax cases conducted by the National Revenue Administration. Its aim was to ascertain whether KAS had conducted its preliminary proceedings correctly and thoroughly during the reorganisation.

Thorough preparation for the reorganisation

During the period under review, the mission of the National Revenue Administration was defined as ensuring stable and efficient public finances and high-quality services. On the one hand, KAS was intended to be a supportive organisation, assisting honest taxpayers and businesses, whilst on the other hand – it was to be efficient and effective in conducting criminal and fiscal criminal proceedings.

The preparations for the reorganisation were thorough – they were preceded by needs assessments, the legislative process for the regulation introducing the changes was smooth, and the directors of the revenue administration chambers generally implemented the changes to the relevant organisational regulations on time. The necessary measures are set out in the recommendations issued by the Ministry of Finance to the directors of the revenue administration chambers on 19 September 2022. They set out the scope of activities, particularly with regard to organisational matters, human resources and IT systems. With a few exceptions, the measures set out in the recommendations have been implemented in all the offices covered by the audit. An analysis of staffing levels was carried out, new job descriptions and authorisations were drawn up, training was provided, and staff in the fiscal criminal affairs units – designated to conduct preliminary proceedings – were granted access to the necessary applications and systems. However, despite the recommendations, not all offices have set up a team or position dedicated to key entities, a decision which was justified, among other things, by the fact that there were too few such entities. In two offices, it was found, amongst other things, that the job descriptions for staff assigned to conduct fine proceedings had been drawn up inaccurately or had not been updated, and that appropriate training had not been provided for some staff members.

Workload in offices

The reorganisation was intended to enable more efficient management of human resources and reduce excessive workloads. One of the tools for effective management was to be a workload assessment model. The Ministry of Finance has undertaken analytical work on its preparation, but this had not been finalised by the time the audit was completed. The heads of offices monitored and analysed the workload in the SKK units and took appropriate action in the event of an uneven distribution of tasks. However, a comprehensive analysis of the workload required taking into account, amongst other things, the significant caseload relating to the Accounting Act, the varying degrees of complexity of the cases, as well as the differing levels of competence and qualifications among staff. On an annual average basis, the figures per employee of the SKK unit for the years 2021–2023 were as follows: 41.1, 33.6 and 35.1 ongoing preliminary proceedings, and 44.4, 38.9 and 32.3 completed preliminary proceedings.

Achieving the planned results

An assessment of the initial effects of the reorganisation was carried out at the Ministry of Finance on the basis of an anonymous and voluntary survey of staff in the SKK units. Respondents mainly reported problems relating to the use of IT systems, including issues with hardware and software. Fewer than one in five respondents (18%) gave a negative assessment of their cooperation with non-designated tax offices in relation to tasks carried out in the area of criminal tax matters. Following the presentation of the survey results, the directors of the revenue administration chambers were obliged to report on the measures taken to improve the functioning of the SKK units following the reorganisation.

In April 2024, an impact assessment of the centralisation of fiscal criminal proceedings was carried out, which showed, amongst other things, that between 2022 and 2023 the number of staff employed in the SKK units fell by 8%, whilst the number of staff authorised to impose fines for fiscal misdemeanours increased by 15%. During the same period, the costs associated with the use of private cars by SKK units rose by 375%, whilst the amounts paid in allowances to SKK unit staff at tax offices increased by 158%. Furthermore, the number of proceedings initiated in cases involving offences under the Accounting Act has risen by almost 100%. The above analysis showed that the intended outcomes of the reorganisation had been achieved. Nevertheless, its negative effects have also been identified.

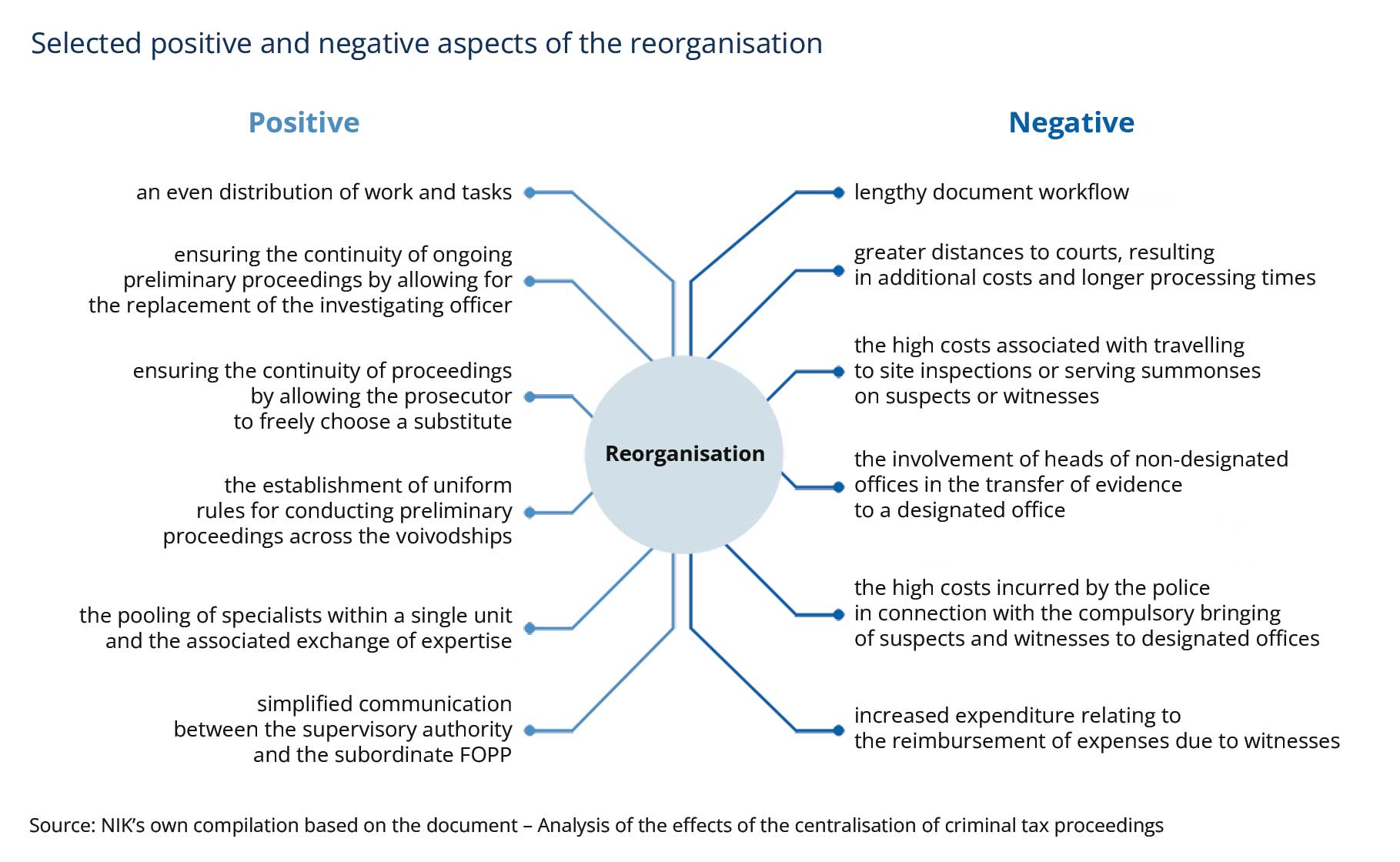

Description of the image

Selected positive and negative aspects of the reorganisation

- The positive aspects of the reorganisation:

- an even distribution of work and tasks

- ensuring the continuity of ongoing preliminary proceedings by allowing for the replacement of the investigating officer

- ensuring the continuity of proceedings by allowing the prosecutor to freely choose a substitute

- the establishment of uniform rules for conducting preliminary proceedings across the voivodships

- the pooling of specialists within a single unit and the associated exchange of expertise

- simplified communication between the supervisory authority and the subordinate FOPP

- The negative aspects of the reorganisation:

- lengthy document workflow

- greater distances to courts, resulting in additional costs and longer processing times

- the high costs associated with travelling to site inspections or serving summonses on suspects or witnesses

- the involvement of heads of non-designated offices in the transfer of evidence to a designated office

- the high costs incurred by the police in connection with the compulsory bringing of suspects and witnesses to designated offices

- increased expenditure relating to the reimbursement of expenses due to witnesses

Source: NIK’s own compilation based on the document – Analysis of the effects of the centralisation of criminal tax proceedings

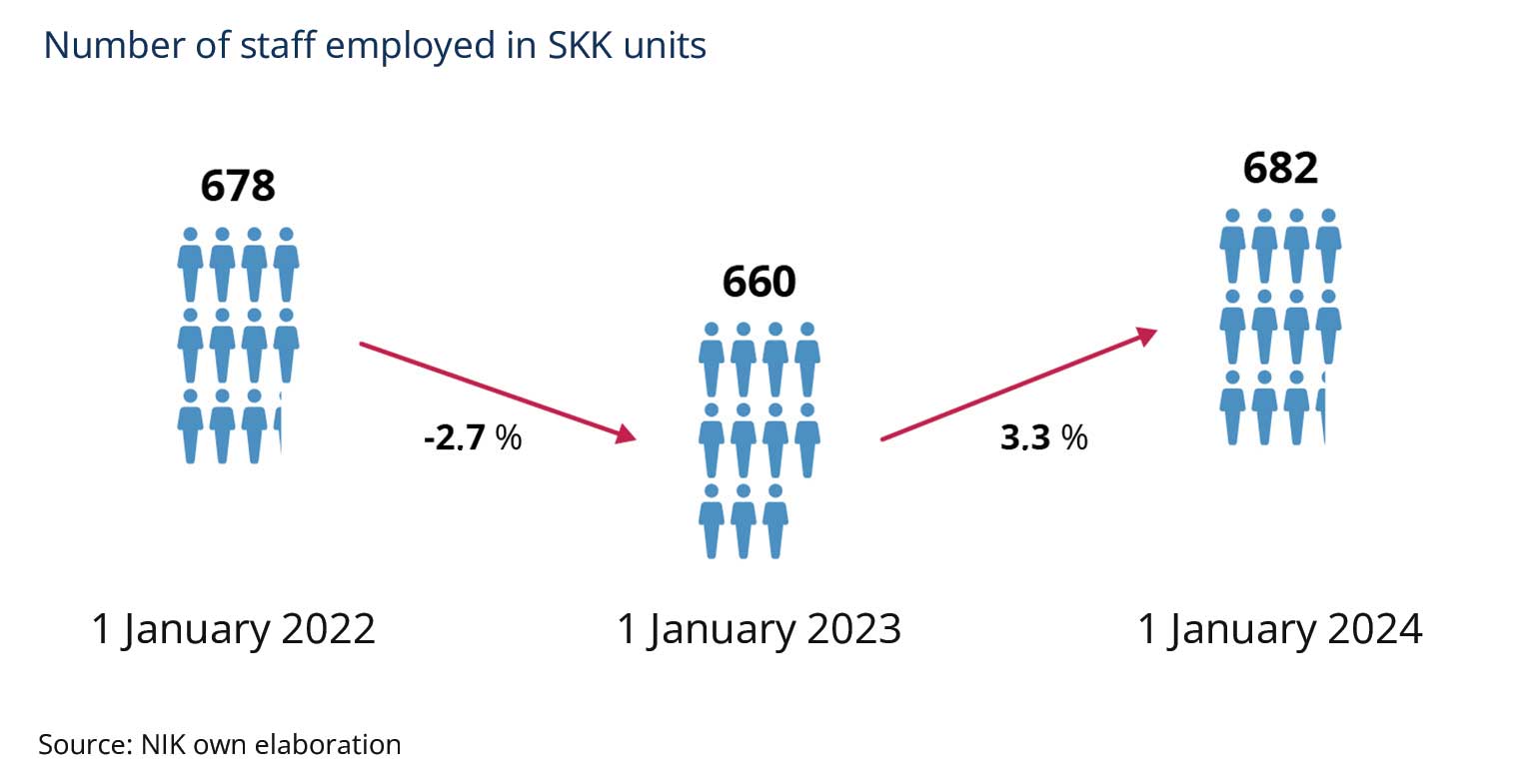

During the period covered by the audit, there were personnel changes within the SKK units. Following an initial 2.7% decline in employment between 1 January 2022 and 1 January 2023, there was a 3.3% increase as of 1 January 2024.

Description of the image

Number of staff employed in SKK units

- As at 01 January 2022 678

- Change: -2.7%

- As at 01 January 2023 660

- Change: 3.3%

- As at 01 January 2024 682

Source: NIK own elaboration

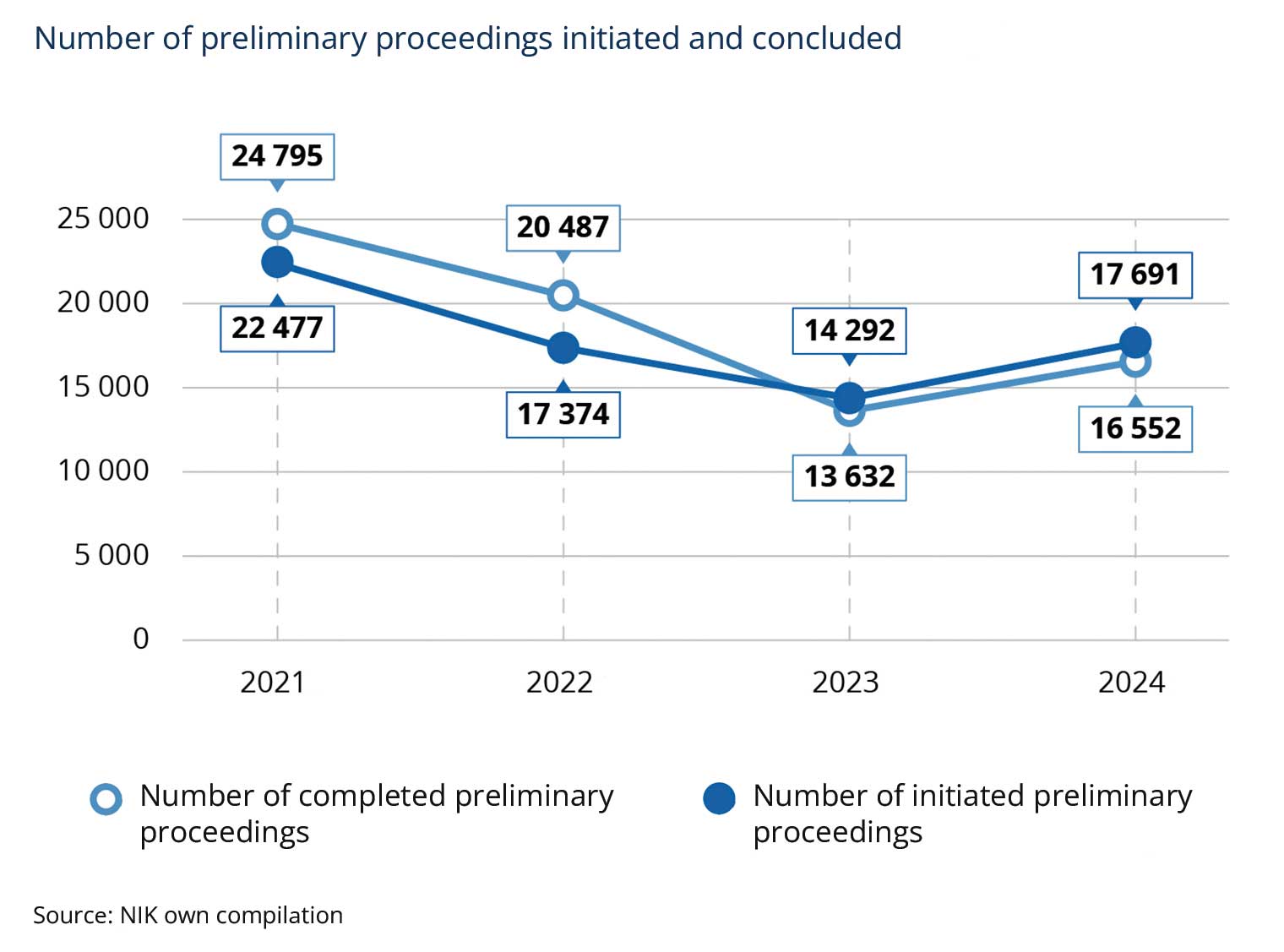

A downward trend in some of the statistics relating to proceedings

The downward trend in the number of preliminary proceedings initiated and concluded between 2022 and 2023 was reversed in 2024, i.e. in the second year of the reorganisation.

It is true that in 2024, compared to the previous year (2023), there was an increase of almost 24% in the number of proceedings initiated and of almost 21% in the number of proceedings concluded, nevertheless, in the first two years of the reorganisation (2023–2024), compared to the preceding years (2021–2022), the total number of proceedings initiated was lower by almost 20%, and those concluded by over 33%. Therefore, trends in this area require monitoring, and the impact of the reorganisation must be analysed in the coming years.

Description of the image

| Year | Number of completed preliminary proceedings | Number of initiated preliminary proceedings |

|---|---|---|

| 2021 | 24,795 | 22,477 |

| 2022 | 20,487 | 17,374 |

| 2023 | 13,632 | 14,292 |

| 2024 | 16,552 | 17,691 |

Source: NIK own compilation

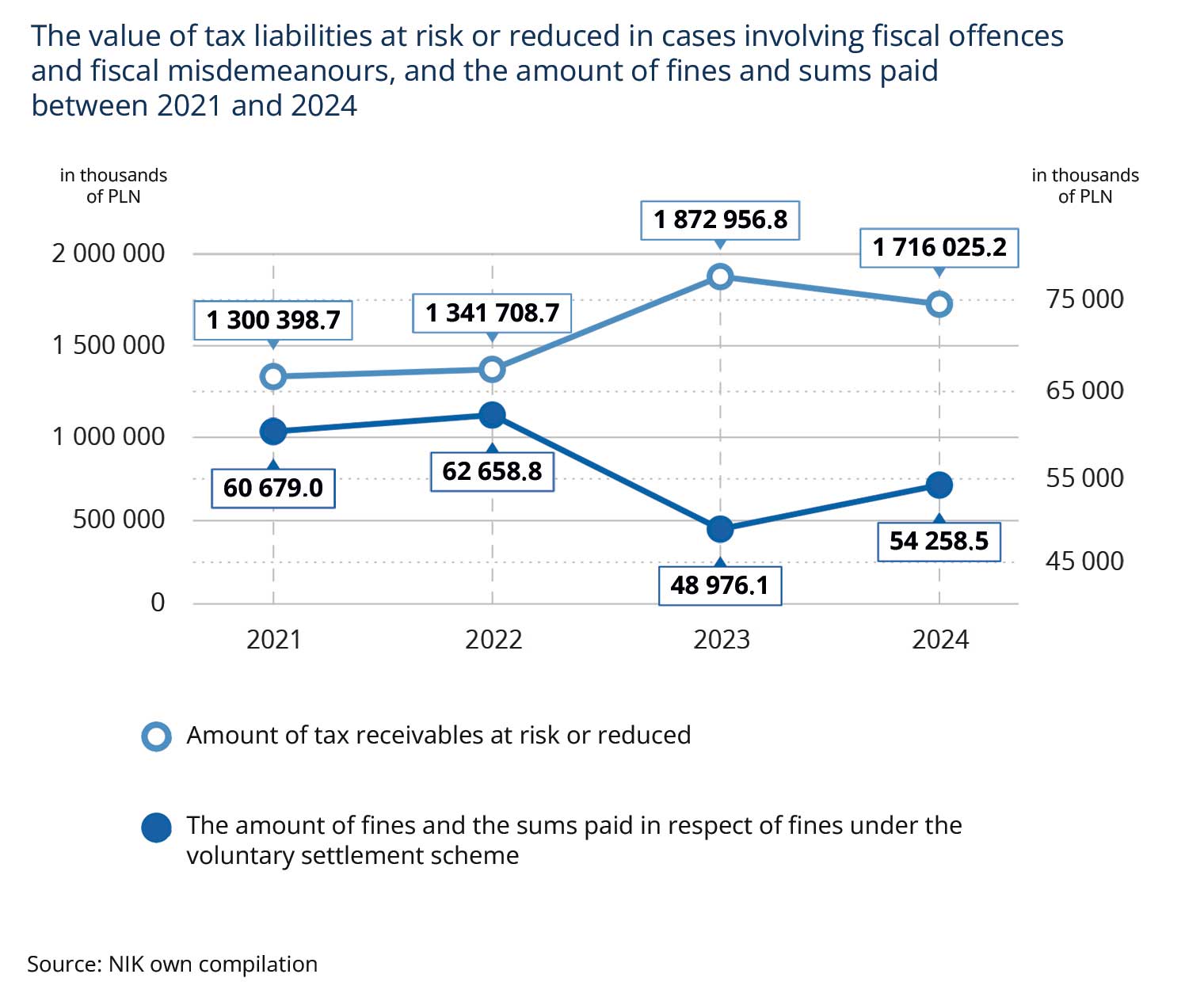

At the same time, the value of tax receivables at risk or reduced in cases involving fiscal offences and fiscal misdemeanours rose by 36%, totalling PLN 6.2 billion between 2021 and 2024. Furthermore, in 2024, this figure fell by more than 8% compared with the previous year (2023). Between 2021 and 2024, the total amount of fines and sums paid under the voluntary settlement scheme amounted to PLN 226.5 million. In 2024, there was an 11% increase compared to 2023, whilst there was a decline of almost 22% between 2022 and 2023.

Description of the image

The value of tax liabilities at risk or reduced in cases involving fiscal offences and fiscal misdemeanours, and the amount of fines and sums paid between 2021 and 2024| Year | Amount of tax receivables at risk or reduced (PLN thousand) | The amount of fines and the sums paid in respect of fines under the voluntary settlement scheme (in thousands of PLN) |

|---|---|---|

| 2021 | 1,300,398.7 | 60,679.0 |

| 2022 | 1,341,708.7 | 62,658.8 |

| 2023 | 1,872,956.8 | 48,976.1 |

| 2024 | 1,716,025.2 | 54,258.5 |

Source: NIK own compilation

Following the reorganisation, the target set out in the annual action and development plan of the National Revenue Administration regarding the proportion of completed preliminary proceedings out of the total number of ongoing proceedings for 2023 and as at the third quarter of 2024 has been achieved. The target for the value of seized assets for 2023 was also achieved, but by the third quarter of 2024 it had not yet been fully met, partly due to the complexity of the cases and the need to carry out additional procedural and operational activities.

Irregularities in the conduct of preliminary proceedings

The audit revealed that, with regard to the grounds for refraining from initiating preliminary proceedings, in four (out of the seven examined) designated offices, the assessment of negative procedural grounds was carried out on the basis of internal regulations that were inconsistent with the provisions of the Fiscal Penal Code. Irregularities were also identified in relation to the unreliable documentation or lack of documentation of: negative procedural grounds identified, legal bases or circumstances taken into account when assessing the existence of negative procedural grounds, as well as instances of irregularities in the decision not to initiate preliminary proceedings or formal irregularities.

The audited authorities did not always conduct proceedings relating to fiscal offences and fiscal crimes correctly; however, in most cases, the irregularities identified were few in number and did not have a significant impact on the activities under audit. Only one of the seven audited offices received a negative rating in this area. The irregularities identified during the audit concerned, amongst other things: delays in initiating proceedings, failure to apply in a timely manner or failure to apply for an extension of the time limit for conducting an investigation into a fiscal offence or a fiscal misdemeanour, allowing the statute of limitations to expire, failing to notify a party to the proceedings of a change in the authority conducting the preliminary proceedings, and the improper conduct of preliminary proceedings (resulting in the premature discontinuation of proceedings where available evidence has not been exhausted, or the court issuing a ruling to refer the case to the head of the office to remedy significant deficiencies), delays in submitting applications to the court for permission to voluntarily submit to liability.

Recommendations

NIK is submitting a proposal de lege ferenda to the Minister of Finance and the Economy to regulate the transfer of materials necessary for conducting preliminary proceedings from non-designated to designated tax offices. It also calls for the effects of the reorganisation to be monitored and analysed in the coming years.

NIK requests the directors of the revenue administration chambers to:

- ensure that decisions are issued regarding the extension of preliminary proceedings and regarding the approval of orders to discontinue, suspend or refuse to initiate such proceedings before the expiry of the time limit within which, pursuant to Article 153 of the Fiscal Penal Code, the proceedings should be concluded;

- remove from current internal regulations the grounds for refraining from initiating preliminary proceedings that are inconsistent with Article 53(7) of the Fiscal Penal Code;

- strengthen oversight of preliminary proceedings conducted by heads of tax offices and ensure that decisions not to initiate such proceedings are made correctly.

NIK requests the heads of the designated tax offices to:

- ensure that applications for the extension of preliminary proceedings, as well as decisions to discontinue, suspend or refuse to initiate such proceedings, are forwarded to the revenue administration chambers for approval before the expiry of the time limit within which, pursuant to Article 153 of the Fiscal Penal Code, the proceedings must be concluded;

- strengthen oversight of representatives of the head of the tax office authorised under Article 118(3) of the Fiscal Penal Code, with regard to the prompt initiation of preliminary proceedings.